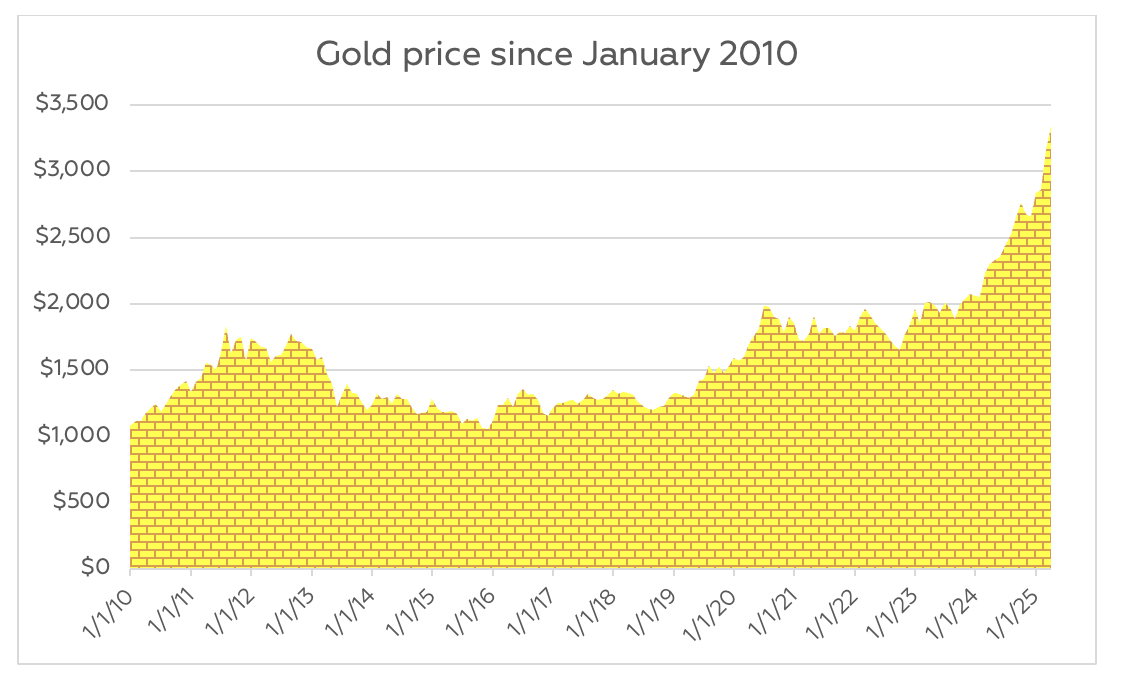

The government wants to encourage investment, not savings.

“For too long, we have presented investment in too negative a light…quick to warn people of the risks, without giving proper weight to the benefits…”

These words may sound like the rhetoric of the chief executive officer of a fund management company, but they are not. In fact, they belong to the Chancellor, Rachel Reeves, and formed part of her recent Mansion House speech. Earlier in her speech, she said, “I am rolling back regulation that has gone too far in seeking to eliminate risk.” For April 2026, she promised a campaign to promote the benefits of retail investment, funded by the financial services industry.

If you have become accustomed to all the small print warnings that accompany almost anything financial, you may be wondering what is going on. Has the government suddenly switched from consumer protection to buyer beware? The answer is no, but:

· The financial services industry is a member of the eight ‘growth-driving sectors’ that formed part of the government’s recently launched 10-year industrial strategy, and the one that falls most clearly into the Chancellor’s remit.

· The UK’s standing in global finance has been declining in recent years, with events like Brexit and the Liz Truss mini-budget calling into question the nation’s financial stability. The current government, like its predecessor, wants to reverse that decline.

· The government does not have the resources to make all the large industrial and infrastructure investments that UK plc requires. Borrowing more to fund the investment – yet alongside raising more tax – would be dangerous, both economically and politically. Consequently, the Chancellor is turning to private investors, both individual and institutional, such as pension funds.

· Rachel Reeves has long been trailing the idea that she wants to “improve returns for savers” by, for example, reducing the amount that can be placed in cash Individual Savings Accounts and pushing pension fund investment in private markets.

The Chancellor clearly has the view that reducing financial regulation and encouraging more risk-taking will be good for the financial services industry and economic growth. It is a strategy which should stimulate more investment, but one that makes professional advice even more important.